Are you thinking about buying a home but feeling overwhelmed by all the options out there? Maybe you’ve heard about private mortgage rates and are wondering if they’re the right choice for you. Or perhaps you’ve had a few roadblocks with traditional lenders and are searching for a way to make your dream of owning a home a reality.

You’re not alone in this journey, and there are ways to make it happen. Private mortgage lenders might just be the key you’ve been looking for. Keep reading to find out how these options can open doors for you — even if your credit history isn’t perfect or if you’re not quite meeting the usual bank requirements

What Are Private Mortgage Rates?

Private mortgage rates refer to the interest rates set by private lenders, such as individuals or smaller lending companies, rather than major banks or credit unions. These lenders operate outside the strict regulations of traditional financial institutions, allowing them to offer more flexible lending solutions.

For those in BC with less-than-perfect credit or difficulties securing a mortgage from a bank, private mortgage lenders provide an alternative path to homeownership. While their rates may be higher than those of traditional lenders, private lending options can offer tailored solutions to meet unique financial situations.

Determining Private Mortgage Rates

Four key factors influence private mortgage rates in BC:

- Loan-to-Value (LTV) Ratio: Lower LTV (e.g., ≤50%) reduces risk and secures better rates. For instance, a $600K home in Vancouver with a 50% LTV may qualify for rates starting at prime + 1.59%* while increasing to prime + 4.25%* at 75% LTV. Higher LTVs mean greater risk, leading to increased interest rates. (Rates spread subject to change)

- Property Value: Higher-value properties often receive better rates as they pose less risk for lenders. A $1M home in Victoria may secure a lower private mortgage rate than a $300K property in a rural area, where the resale potential is lower.

- Credit & Income Verification: While private lenders are more flexible, some of them might still assess creditworthiness. Borrowers with strong credit (680+ score) and verifiable income can access lower rates, whereas those with poor credit or stated income may see rates increase by 1-2%.

- Market Conditions: Private mortgage rates fluctuate based on economic factors like Bank of Canada rate changes, inflation, and local housing demand. A stable market with low vacancy rates can lead to more competitive private lending terms, while uncertainty may push rates higher.

Unlock Your Path to Homeownership! Don’t let traditional lenders hold you back. Learn more about private mortgage options and get the best rates with expert guidance!

How Private Mortgage Rates Work

Private mortgage rates differ from traditional bank rates because private lenders operate with more flexibility and fewer regulatory constraints. This allows them to approve borrowers who may not meet the strict credit or income requirements of conventional lenders.

Since private mortgage lenders take on more risk, their interest rates tend to be higher than bank rates. However, they offer key advantages, such as faster approval times, customized private mortgage loan rates and terms, and greater flexibility in assessing your financial situation. If you need quick funding or have unique circumstances—such as self-employment or a low credit score—private mortgage rates may be a worthwhile tradeoff for easier access to financing

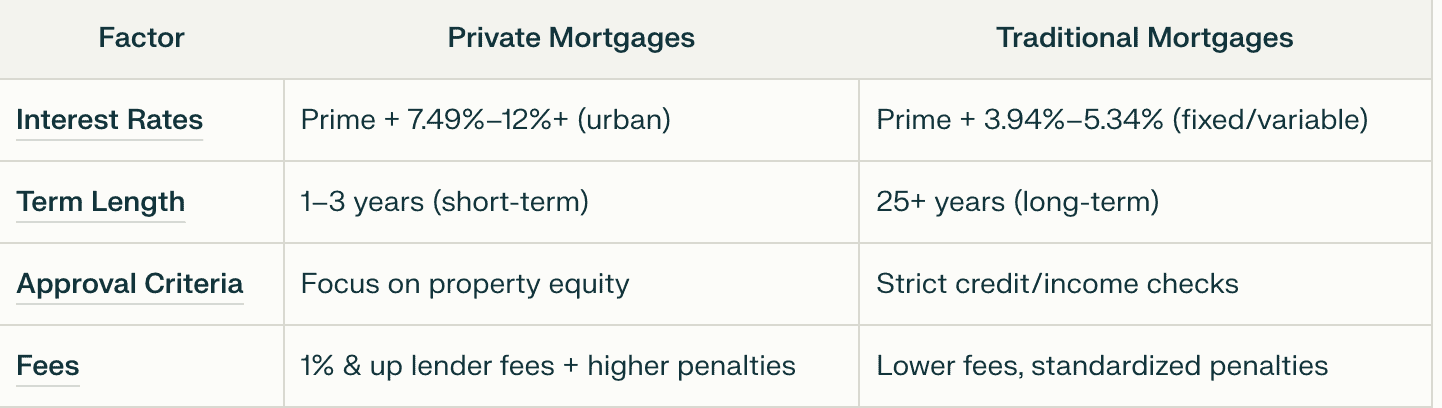

Private Mortgage Rates vs. Traditional Mortgage Rates BC

You might be wondering, “How do private mortgage rates in BC compare to traditional mortgage rates from a bank?” Here’s the breakdown:

Traditional Mortgages in BC:

- Lower Interest Rates: Banks typically offer lower rates (e.g., 5-6%) because they lend to borrowers with strong credit and stable income.

- Strict Eligibility: Securing a traditional mortgage in BC can be difficult if you have bad credit, irregular income, or a high debt load.

- Longer Process: Bank approvals can take weeks or months, requiring extensive paperwork and strict underwriting.

Private Mortgages in BC:

- Higher Interest Rates: Private lenders charge higher rates (typically 7-12%) but offer flexibility and alternative financing options.

- More Flexible Terms: Unlike banks, private lenders in BC consider self-employed individuals, borrowers with lower credit scores, and those needing short-term solutions.

- Faster Approval: Many private lenders in British Columbia can approve mortgages in days instead of weeks, making them ideal for urgent financing needs.

The Pros and Cons Of Private Mortgages

Opting for a private mortgage in BC has its advantages, but there are also potential drawbacks to consider. Here’s a breakdown of the pros and cons:

Pros:

- Flexibility in Terms – Private lenders in BC accommodate non-traditional income sources, lower credit scores, and unique properties, making homeownership accessible to more borrowers.

- Faster Approval – Unlike banks, private mortgage approvals can happen in a matter of days, making them ideal for urgent purchases or refinancing needs.

- Tailored Loan Solutions – Borrowers can access custom loan structures, such as interest-only payments or shorter-term loans, to suit their financial goals.

- Less Strict Credit Requirements – Even with bad credit, private lenders focus on the property’s value and income potential rather than just credit history.

- Access to Second Mortgages – Homeowners in BC can leverage their home equity for additional financing, which may not always be an option through traditional banks.

Cons:

- Higher Interest Rates – Private mortgage loan rates are typically prime + 1.59%* to prime + 4.25%* compared to traditional bank rates of 5-6%, making them more expensive over time.

- Shorter Loan Terms – Many private mortgages in BC are short-term (6 months to 3 years), requiring borrowers to refinance or pay off the loan sooner.

- Higher Fees – Borrowers often face private mortgage lender fees, broker fees, and legal costs, which can increase the overall loan expense.

- Potential for Higher Risk – If unable to refinance or pay off the loan within the term, borrowers may face renewal challenges or foreclosure risks.

- Limited Loan Amounts – Private lenders may impose lower borrowing limits compared to banks, depending on the property location and loan-to-value ratio.

How a Mortgage Broker Can Help You Secure Private Financing in BC

Working with a licensed mortgage broker specializing in private lending can streamline the process and help BC borrowers secure better terms. At our mortgage brokerage, we leverage our network to:

- Access competitive rates (prime + 1.59%* to prime + 4.25%*) from MICs, family offices, and accredited investors.

- Negotiate private mortgage lender fees (typically 1% and up) and minimize prepayment penalties.

- Fast-track approvals within 24–72 hours for urgent purchases or refinancing.

- Navigate BC-specific regulations, including FSRA licensing tiers for private mortgage activity.

We provide equity-based solutions (up to 75% LTV) for credit-challenged borrowers and develop strategic exit plans to transition to traditional financing within 1–3 years. Unlike banks, we prioritize property value over credit scores, making private lending accessible to self-employed borrowers and those facing tax arrears.

In BC’s high-cost markets—such as Vancouver and Victoria—we secure emergency funding to stop the power of sale proceedings and redeem foreclosures, ensuring compliance with provincial lending laws.

Is Private Mortgage Lending the Right Fit for You?

Private mortgages are a practical short-term solution for BC borrowers who don’t meet traditional lending criteria. They provide fast approvals and flexibility, making them ideal for self-employed individuals, those with credit challenges, or buyers needing quick financing. Working with a licensed BC mortgage broker can help you secure better terms, minimize fees, and ensure a smooth transition to long-term financing. If you’re exploring private lending options in BC, reach out to us for expert guidance.

Get Personalized Mortgage Solutions Today! Ready to explore flexible private mortgage rates? Contact us now to find the perfect financing option tailored to your needs!

FAQs

How can a private mortgage broker help?

A private mortgage broker helps borrowers navigate the private mortgage market by connecting them with suitable private lenders. They work with a variety of lenders, including the top private mortgage lenders, and can negotiate better terms for clients, making the process smoother and more efficient.

Are private mortgage rates fixed or variable?

Private mortgage rates can be either fixed or variable, depending on the lender. Some private mortgage lenders offer fixed rates for stability, while others provide variable rates that fluctuate with market conditions.

How do private mortgage loan rates compare to traditional lending options?

Private mortgage loan rates are typically higher than those from banks or credit unions but may be lower than some alternative lending options like payday loans or unsecured personal loans. The exact rate depends on factors such as the loan-to-value (LTV) ratio, property location, and borrower risk profile.

Can I negotiate private mortgage lender fees?

Yes, borrowers can sometimes negotiate private mortgage lender fees, especially if they work with a mortgage broker. Common fees include broker fees, loan origination fees, and legal fees. Reducing or spreading out these costs can make the loan more affordable.

What are the repayment terms for private mortgage loans?

Repayment terms vary, but most private mortgage loans are short-term, ranging from six months to three years. Borrowers often refinance into a traditional mortgage before the term ends.