Home Equity Loan vs. Home Equity Line of Credit

Wondering what to choose between a home equity loan vs a home equity line of credit (HELOC)? Your search for answers is over!

As your most trusted mortgage broker in Vancouver, we do as much as we can to help our clients make informed decisions in using their home equity. In this article, we included everything you need to know about the main differences between a home equity loan and a home equity line of credit.

So let’s dig in!

Do you need money for a home improvement project, to consolidate debt, bridge loan, book a family holiday, or to pay your kids’ college tuition?

If you are a homeowner in BC, Canada, needing to finance a large or unexpected expense, your home equity’s value gives you two borrowing options: to get a home equity loan, or a home equity line of credit (HELOC).

With interest rates typically lower than other types of financial options (like credit cards or personal loans), these financial products are commonly called second mortgages.

But which one is better for you and your family?

Deciding to borrow against the equity in your home is not a decision to be taken lightly.

The key to knowing which one to choose between a home equity loan vs a home equity line of credit, is thoroughly understanding the pros and cons for each one.

Advantages and Disadvantages of Home Equity Loans

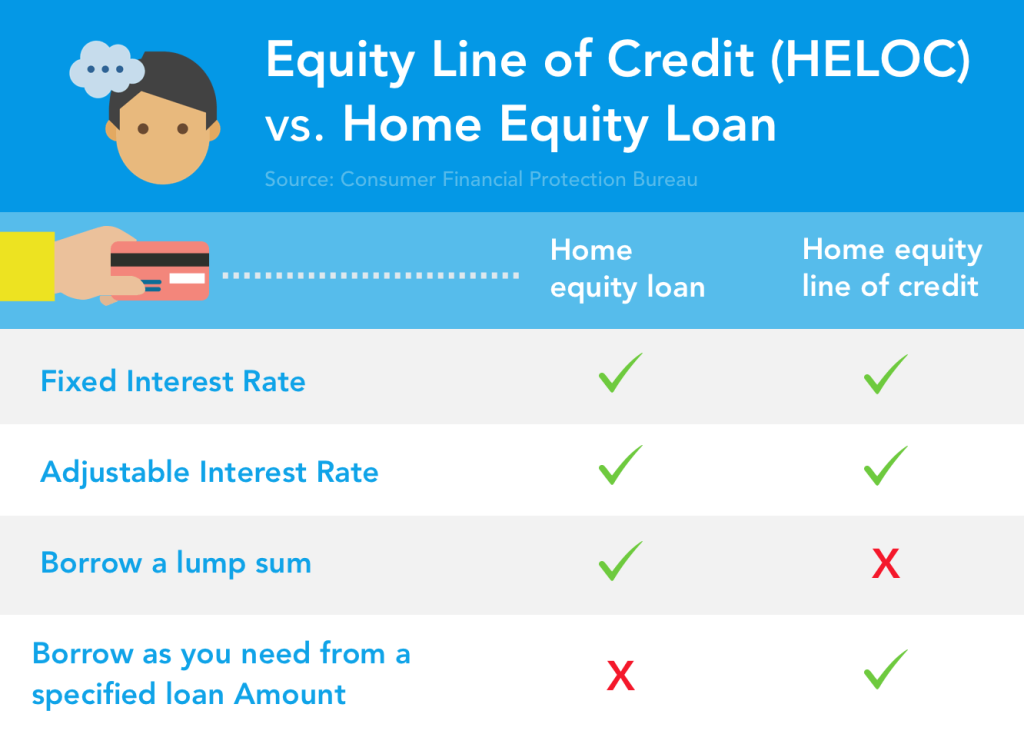

How is a HELOC the same as a home equity loan?

Both these types of loans use your home as a collateral just like mortgages do. But that’s pretty much all they have in common!

The main difference between home equity loans and home equity lines of credit is that a home equity loan allows you to borrow all the money at once.

Like conventional loans, a home equity loan comes with fixed monthly payments, interest rates and repayment terms. These make them a more secure and predictable option than HELOCs. Knowing how much you owe each month throughout the entire life of the loan, and the amount of money you need to pay back at the end can be comforting for many. That’s even more the case during such an unstable economic and financial climate during the 2020 pandemic.

Except for predictability, one more added benefit of this financial tool is that the interest you pay on the loan may be tax deductible.

An important part though when deciding between a home equity loan vs a home equity line of credit is the financial institution you plan to address.

With banks or credit unions, the credit limit you can borrow will be usually limited by a loan to value and income ratio. Except for the appraised value of your home, this ratio also takes into account your income situation, credit history or credit score report. And because of the COVID-19 pandemic and the resulting financial shock, banks’ approvals are even tougher. This makes it hard for many property owners to qualify for the loan they need.

When working with a reputable mortgage broker in BC, no other factors other than how much equity you have added in home matter. Our selected private lenders in Vancouver have plenty of loan options for everyone. Their solutions suit any borrower’s financial situation, even the most complicated ones.

And now for the best part: some of our lenders will not charge you a prepayment penalty in case you want to pay off your loan ahead of schedule, like most banks usually do.

Advantages and Disadvantages of Home Equity Lines of Credit

When looking at what to choose between a home equity loan vs a home equity line of credit, you should know that HELOCs work like credit cards.

A HELOC will give you access to a line of credit so that you can borrow as little or as much as you need. In the end, you will only need to repay the amount you had used.

This financial tool has two periods, a draw period and a repayment period, and variable rates which can remain low or not, depending on index fluctuations.

And if you wonder what an index fluctuation includes, it can be factors like how much you borrow, your interest rate and the market’s volatility.

In most cases, the smallest monthly payments will cover the interest during the draw period. But since different lenders have different offers, for some HELOCs you will need to pay a large lump sum at the end.

When comparing the differences between a home equity loan and a home equity line of credit, this type of loan has one major benefit: flexibility. HELOCs can be used for anything you want, but are better suited for home repairs and renovation which can raise your home’s value.

Like in the case of home equity loans, private lenders saw the potential here too. Many individuals that banks refuse, are well capable of repaying their loans. That’s why, if you’re looking for how to get a HELOC with no income or with a weaker credit score, our B-lenders in BC can help you with that too.

Understanding financial products can be tricky and choosing one may require the advice of an experienced financial advisor. So why not contact us today and we can discuss your situation in depth. We can decide together which product is better suited for you between a home equity loan vs a home equity line of credit. We can also guide you towards the best lender with the most affordable terms and conditions.